I want to solve my problem I couldent found Varmax function could you help me

Look up the teradata package to see if it helps.

install the "astsa" package ----

install.packages('astsa')

library(astsa)

#Load the data set, and parametrize the different set sizes.----

lap_df <- as.data.frame(lap)

nData <- nrow(lap_df)

nShortData <- nData - 52

#Add "seqid" and "id" columns to prepare the data frame for use with the VARMAX function----

seqid <- rep(1, nData)

id <- seq(1:nData)

lap_df_indexed <- cbind(seqid, id, lap_df)

#Create a table in the database to hold the data.

install.function('copy_to')

install.packages("dplyr")

install.packages("dbplyr") # For database interaction

install.packages("DBI") # For database connections

install.packages("RSQLite") # Example database backend

library(dplyr)

library(dbplyr)

library(DBI)

library(RSQLite)

help('copy_to')

??copy_to

con <- DBI::dbConnect(RSQLite::SQLite(), ":memory:")

copy_to(con, lap_df_indexed, name="lap_data", overwrite=TRUE)

#Create a tibble for the main data set.

tddf_lap_data <- tbl(con, "lap_data")

#Obtain the shortened data by using the first nShortData

df_lap_data <- as.data.frame(tddf_lap_data)

df_lap_data_short <- df_lap_data[1:nShortData,]

copy_to(con, df_lap_data_short, name="lap_data_short", overwrite=TRUE)

tddf_lap_data_short <- tbl(con, "lap_data_short")

#Perform the VARMAX analysis with

help.search("td_varmax_mle")

install.packages("sos")

library(sos)

install.packages("astsa")

library(astsa)

library(devtools)

lap_varmax <- td_varmax_mle(

data = tddf_lap_data_short,

response.columns = c("cmort","tempr","part"),

partition.columns = c("id"),

orders = "1, 0, 1",

step.ahead = 52,

data.partition.column = c("seqid"),

data.order.column = c("id")

)

these codes from terar data it give me error

Error in td_varmax_mle(data = tddf_lap_data_short, response.columns = c("cmort", :

could not find function "td_varmax_mle"

You don't seem to have installed a package that includes td_varmax_mle. The function is mentioned in teradata, but the documentation I found is a little odd so I don't know if it will help.

i cand found function while i was installed the package

Which package did you install that includes the function?

Many packages

astata

Vars

MTS

MARRS

I searched from chat Gpt any thing written I installed but it doesn't work

Also I am work on varmax for the first time so I can fixed

? If I can't how should I do

Do any of those packages do VARMAX? My guess is "no," but I don't know for sure.

I need for my master

It is possible that you need to use a different piece of software.

It is my impression that VARMAX models are not widely used, so you might consider an alternative such as VARX.

Or you might just do equation-by-equation ARMAX which will give you basic VARMAX estimates. You might have to do some more work then to use the estimates.

I want to forecast my data,

Can I use matlab or python which one give me correct varmax model for forcasting

I believe you can do it in Python. Not sure about Matlab. Or you could forecast with equation-by-equation ARMAX in R with a little extra work.

it means i cant do it by R at all , no one didi it by R

hello sir,

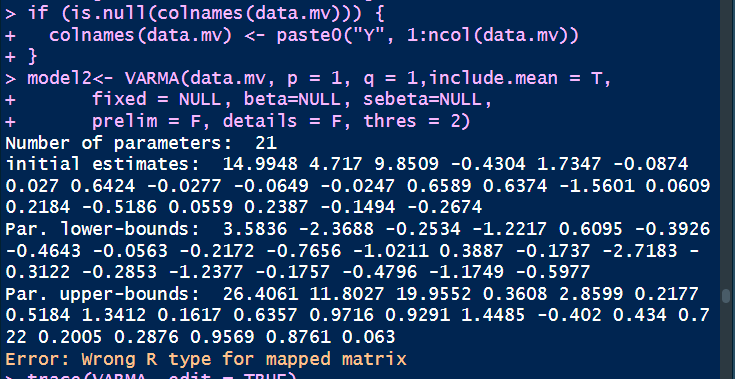

i am really sorry to take your time , I have found VARMA model and just for 2Y i have 3Y and the Error is attached below also i attached my code ,

could you please help me?

I will be very happy to see the results.

(Attachment varmax learn.R is missing)

(Attachment learn2.R is missing)

It may help if you can post a reprex.

Hello sir,

could you check this for me? i want to know if I can use this as Varmax Function

install.packages("MARSS")

library(MARSS)

Simulate multivariate time series

set.seed(123)

n <- 100

exog <- 0.5 * (1:n) + rnorm(n, 0, 1) # Exogenous variable

Generate two time series with ARMA structure

series1 <- arima.sim(list(order = c(1, 0, 1), ar = 0.5, ma = -0.4), n = n)

series2 <- arima.sim(list(order = c(1, 0, 1), ar = 0.4, ma = 0.3), n = n)

Combine data into a matrix

Y <- rbind(series1, series2)

Exogenous variable

X <- matrix(exog, nrow = 1, ncol = n)

Define MARSS model structure

model_list <- list(

B = "unconstrained", # AR component (VAR)

U = "zero", # No deterministic trend

Q = "diagonal and unequal",# State noise covariance

Z = diag(2), # Observation matrix

A = "zero", # No intercept in observation equation

R = "diagonal and unequal",# Observation noise covariance

C = matrix(1, nrow = 2), # Exogenous coefficient matrix

c = X # Exogenous variable

)

Fit the MARSS model

fit <- MARSS(Y, model = model_list)

Summarize results

summary(fit)

I haven't used that package, so I can't advise. You've set up some trial data and estimated it. Did you get back the right values for the coefficients?

I don't know the values right,

Thanks for your support, I should study more on it