Hello R-community! I am using VAR, I want to forecast how my variable "Arbeidsledighet", which means Unemployement is playing out while having a "shock" in my other variable, "Oljepris" which basically means Oilprice. I understand that I have to use VAR, and impulse response function.

I have this dataset:

> Arbeidsledige_KvartL

# A tibble: 36 x 3

kvartal arbeidsledige oljepris

<date> <dbl> <dbl>

1 2011-03-01 74190 115.

2 2011-06-01 65487 114.

3 2011-09-01 65254 113.

4 2011-12-01 63655 108.

5 2012-03-01 67669 125.

6 2012-06-01 64196 95.2

7 2012-09-01 63060 113.

8 2012-12-01 62569 108.

9 2013-03-01 69969 108.

10 2013-06-01 66596 103.

# … with 26 more rows

Then I did:

> attach(Arbeidsledige_KvartL)

> Arbeidsledige=diff(arbeidsledige)

> Oljepris=diff(oljepris)

> arb=cbind(Arbeidsledige, Oljepris)

> library(vars)

> model <- VAR(arb, p = 2, type ="const")

> summary(model)

VAR Estimation Results:

=========================

Endogenous variables: Arbeidsledige, Oljepris

Deterministic variables: const

Sample size: 33

Log Likelihood: -446.499

Roots of the characteristic polynomial:

0.5021 0.1081 0.1081 0.02156

Call:

VAR(y = arb, p = 2, type = "const")

Estimation results for equation Arbeidsledige:

==============================================

Arbeidsledige = Arbeidsledige.l1 + Oljepris.l1 + Arbeidsledige.l2 + Oljepris.l2 + const

Estimate Std. Error t value Pr(>|t|)

Arbeidsledige.l1 -0.38853 0.18833 -2.063 0.0485 *

Oljepris.l1 -124.36834 67.41236 -1.845 0.0757 .

Arbeidsledige.l2 0.01194 0.17212 0.069 0.9452

Oljepris.l2 -23.80439 70.60770 -0.337 0.7385

const -409.51564 775.97023 -0.528 0.6018

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 4296 on 28 degrees of freedom

Multiple R-Squared: 0.2396, Adjusted R-squared: 0.131

F-statistic: 2.206 on 4 and 28 DF, p-value: 0.09408

Estimation results for equation Oljepris:

=========================================

Oljepris = Arbeidsledige.l1 + Oljepris.l1 + Arbeidsledige.l2 + Oljepris.l2 + const

Estimate Std. Error t value Pr(>|t|)

Arbeidsledige.l1 -3.748e-04 5.339e-04 -0.702 0.488

Oljepris.l1 -2.165e-01 1.911e-01 -1.133 0.267

Arbeidsledige.l2 2.517e-05 4.879e-04 0.052 0.959

Oljepris.l2 -3.958e-02 2.002e-01 -0.198 0.845

const -1.811e+00 2.200e+00 -0.823 0.417

Residual standard error: 12.18 on 28 degrees of freedom

Multiple R-Squared: 0.06488, Adjusted R-squared: -0.06871

F-statistic: 0.4856 on 4 and 28 DF, p-value: 0.7461

Covariance matrix of residuals:

Arbeidsledige Oljepris

Arbeidsledige 18458084 -6812.8

Oljepris -6813 148.3

Correlation matrix of residuals:

Arbeidsledige Oljepris

Arbeidsledige 1.0000 -0.1302

Oljepris -0.1302 1.0000

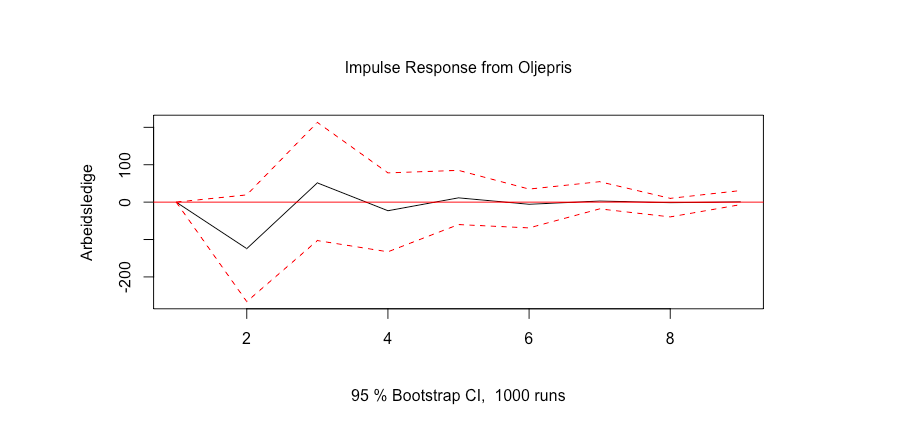

Then I tried to plot it, and wanted to forecast how Arbeidsledighet/Unemployement plays out, when Oilprice is going down:

> feir <- irf(model, impulse ="Oljepris", response ="Arbeidsledige", n.ahead = 8, ortho = FALSE, runs = 1000)

> plot(feir)```

Then I got this plot:

So did I do it right? If not, what should I do, and what did I do wrong? How do I interpret this?