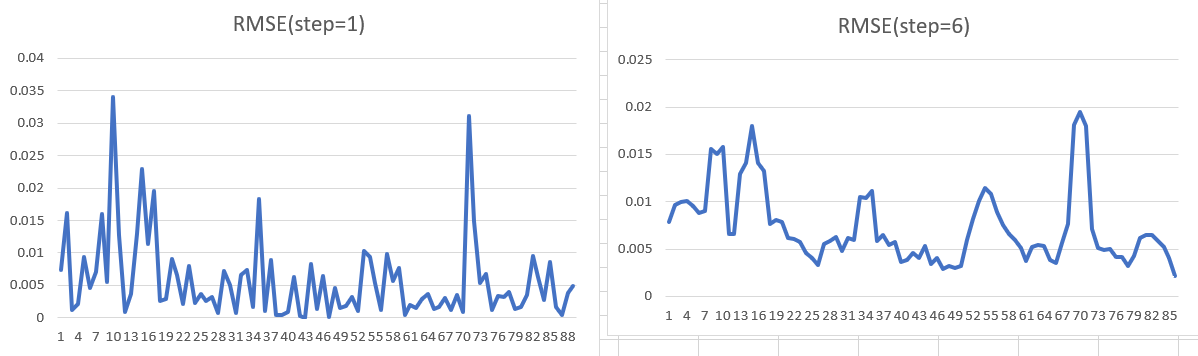

I am using the sliding_window() or rolling_origin() from resample R package . For the one-step-ahead forecast, I used assess = 1, and six steps ahead forecast assess = 6. First, I tune the models then passed these tuned models to fit_resamples() . Get the RMSE from these slices and plot against the time. However, the issue is that I get a larger RMSE at assess= 1 than assess = 6 which is counter-intuitive obviously it should be a larger RMSE at assess =6. I have given below reproducible codes with hypothetical data and graphs. I do not know what is wrong. Is there is an issue with my method? Please help.

library(Quandl)

library(tidymodels)

library(resample)

library(tidyverse)

library(lubridate)

library(timetk)

df1 <- Quandl(code = "FRED/PINCOME",

type = "raw",

collapse = "monthly",

order = "asc",

end_date="2017-12-31")

df2 <- Quandl(code = "FRED/GDP",

type = "raw",

collapse = "monthly",

order = "asc",

end_date="2017-12-31")

per <- df1 %>% rename(PI = Value)%>% select(-Date)

gdp <- df2 %>% rename(GDP = Value)

data <- cbind(gdp,per)

data1 <- tk_augment_differences(

.data = data,

.value = GDP:PI,

.lags = 1,

.differences = 1,

.log = TRUE,

.names = "auto") %>%

select(-GDP,-PI) %>%

rename(GDP = GDP_lag1_diff1,PI = PI_lag1_diff1) %>%

drop_na()

lag_period <- c(1:5)

data_pre_full <- data1 %>%

# add lags

tk_augment_lags(

.value = GDP:PI,

.lags = lag_period)

data_prepared_tbl <- data_pre_full %>%

dplyr :: select( -PI ) %>%

drop_na()

splits <- timetk::time_series_split(data_prepared_tbl, assess = 70, cumulative = TRUE)

recipe_spec <- recipe(GDP ~ ., data = training(splits)) #%>%

# *Resampling-----

resamples_tscv <- sliding_window(data_prepared_tbl,

lookback = 100,

assess_stop = 1, step = 2

)

plan_org <- resamples_tscv %>% tk_time_series_cv_plan()

plan_tr1 <- plan_org %>%

filter(plan_org$.key == "testing")

plan <- plan_tr1 %>% select(Date,.key,.id,GDP)

# * SVM ----

wflw_fit_svm <- workflow() %>%

add_model(

spec = svm_rbf(mode = "regression") %>% set_engine("kernlab")

) %>%

add_recipe(recipe_spec %>% update_role(Date, new_role = "indicator")) %>%

fit(training(splits))

# Fit resamples

keep_pred <- control_resamples(save_pred = TRUE, verbose = TRUE)

set.seed(20201024)

# Fit resamples

rf_res <- fit_resamples(wflw_fit_svm,

resamples = resamples_tscv, control = keep_pred)

rf_res

pr <- rf_res %>%

# grab specific columns and resamples

pluck(".predictions")

pred1<- rf_res %>%

# combine ALL predictions

collect_predictions()

pred_final1 <- cbind(pred1,plan)

write.csv(pred_final1, file = "pred.SVM1.csv")

# Summarize all metrics

rf_res %>%

collect_metrics(summarize = TRUE)

rmse <- rf_res %>% collect_metrics(summarize = FALSE)

rm <- rmse %>%

filter(rmse$.metric == "rmse")

write.csv(rm, file = "rmse_1.csv")