Howdy. Other than the setup, this isn't really an R or RStudio question. But happy to help. It's been 8 years for me spending much time with Greene

The model setup by eq 10-40 is, I think:

costdata = read.csv(".../TableF10-2.csv")

# setup dependent vars for /delta_...

costdata = costdata %>%

mutate(

lnpkpm = log(Pk / Pm),

lnplpm = log(Pl / Pm),

lnpepm = log(Pe / Pm)

)

setup eq 10-40:

df_pooledreg <-

bind_rows(

tibble(

y = costdata$K,

k = 1,

l = 0,

e = 0,

kk = costdata$lnpkpm,

kl = costdata$lnplpm,

ke = costdata$lnpepm,

ll = 0,

le = 0,

ee = 0,

year = costdata$Year

),

tibble(

y = costdata$L,

k = 0,

l = 1,

e = 0,

kk = 0,

kl = costdata$lnpkpm,

ke = 0,

ll = costdata$lnplpm,

le = costdata$lnpepm,

ee = 0,

year = costdata$Year

),

tibble(

y = costdata$E,

k = 0,

l = 0,

e = 1,

kk = 0,

kl = 0,

ke = costdata$lnpkpm,

ll = 0,

le = costdata$lnplpm,

ee = costdata$lnpepm,

year = costdata$Year

)

)

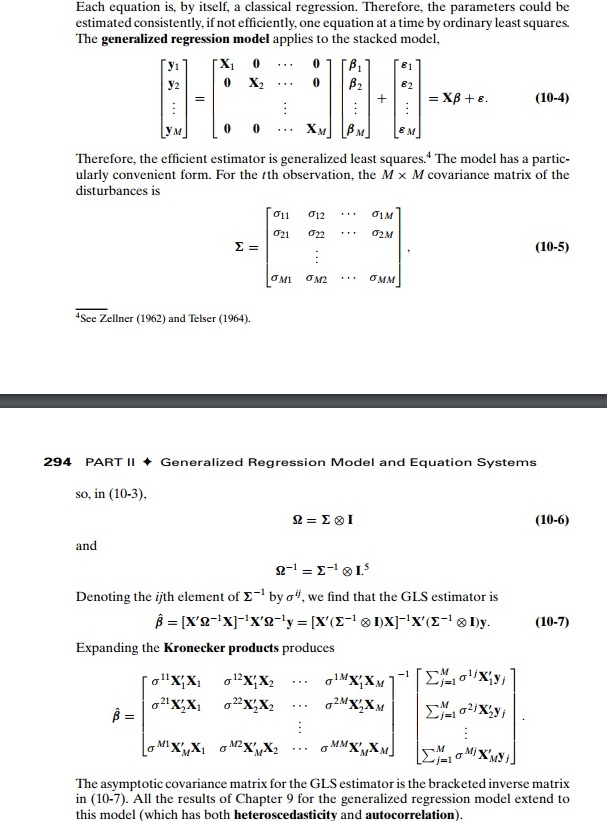

run "The Pooled Model" eq 10-19 in Greene chapter 10.

Note, eq 10-19 doesn't have an intercept.

pooledreg = glm(

y ~ 0 + k + l + e + kk + kl + ke + ll +le + ee,

data = df_pooledreg

)

summary(pooledreg)

I get the following coefficients:

Coefficients:

Estimate Std. Error t value Pr(>|t|)

k 0.056223 0.001888 29.773 < 2e-16 ***

l 0.253409 0.001852 136.834 < 2e-16 ***

e 0.041861 0.002291 18.272 < 2e-16 ***

kk 0.030426 0.008067 3.772 0.000349 ***

kl 0.001755 0.004556 0.385 0.701342

ke -0.003562 0.007481 -0.476 0.635562

ll 0.075127 0.005280 14.228 < 2e-16 ***

le 0.003252 0.005756 0.565 0.574043

ee 0.046777 0.017415 2.686 0.009136 **

---

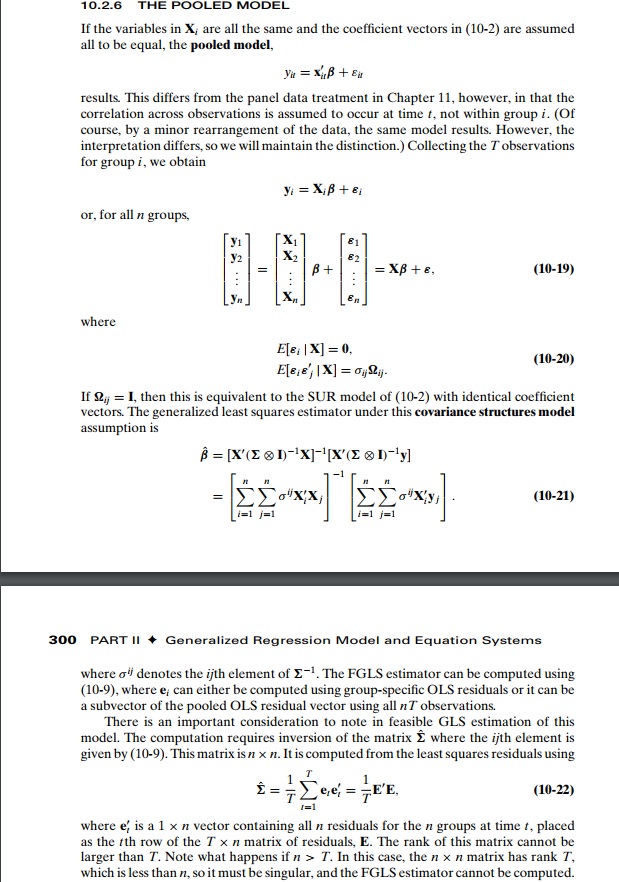

Now, Table 10.4. The first line, Fitted shares is just:

fitted_k = predict(

pooledreg,

df_pooledreg %>% filter(year == 1959 & k)

)

fitted_l = predict(

pooledreg,

df_pooledreg %>% filter(year == 1959 & l)

)

fitted_e = predict(

pooledreg,

df_pooledreg %>% filter(year == 1959 & e)

)

# Note that assuming a constant returns to scale production function,

# `m` is just `1-(k+l+e) `

fitted_m = 1 - (fitted_k + fitted_l + fitted_e)

fitted_k: 0.05655583

fitted_l: 0.2747627

fitted_e: 0.04487152

fitted_m: 0.6238099

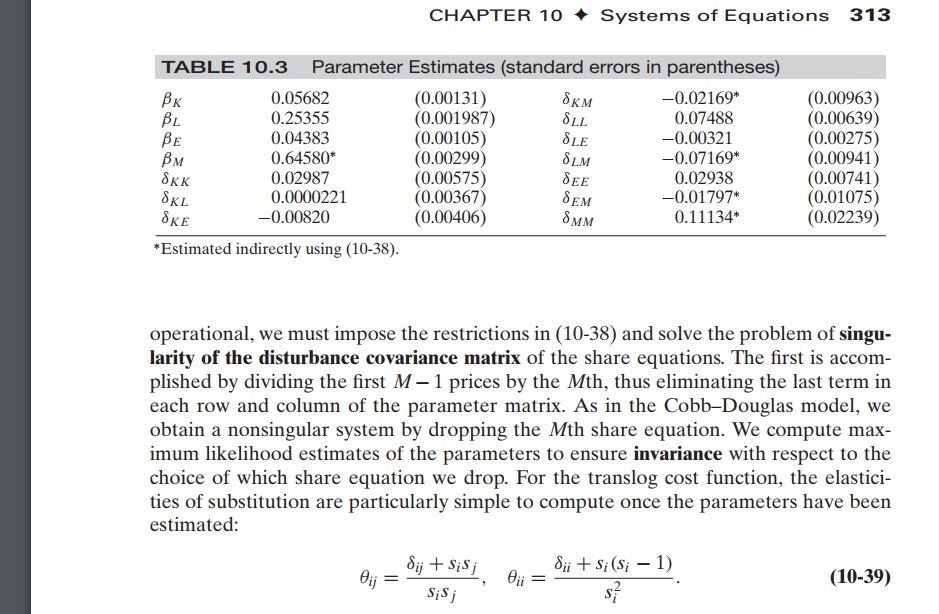

How do we estimate the derivatives involving Materials? i.e. those $/delta_{M...}$? For that, turn to equation 10-38 (well, it's eq 10-38 in my Greene, 6th edition of econometric analysis anyway. they seem to be moving things around). That equation just says,

$\Sigma_{i=1}^M \delta_{ij} = 0$ and $\Sigma_{j=1}^M \delta_{ij} = 0$.

Really simple, you can see this in table 10.4. It just says that $\delta_{KK} + $\delta_{KL} + $\delta_{KE} + $\delta_{KM} = 0.

You'll notice in table 10.4 any derivative with an M has an asterisks next to it, referring to eq 10-38.

Equation 10-39 gives the own and cross elasticities of substitution.

So with $\theta_{kk}$ for example, (/delta_{kk} + s_{i}(s_{i} - 1)) / s_{i}^2, where i is capital share's output in that year.

or with my estimates and your data:

s_k1959 = ((costdata %>% filter(Year == 1959)))$K

delta_kk = pooledreg$coefficients['kk'] %>% as.vector

(delta_kk + s_k1959 * (s_k1959 - 1)) / (s_k1959^2)

[1] -7.214395 # that's under "Implied Elasticities of Substitution, 1959" for Capital/Capital

And for cross price elasticity of substitution, eq 10-39 says

$\theta_{ij}$ is , (/delta_{ij} + s_{i} * s{j}) / (s_{i} * s_{j}),

for example for $\theta_{KL}$:

s_k1959 = ((costdata %>% filter(Year == 1959)))$K

s_l1959 = ((costdata %>% filter(Year == 1959)))$L

delta_kl = pooledreg$coefficients['kl'] %>% as.vector

(delta_kl + (s_k1959 * s_l1959)) / (s_k1959 * s_l1959)

[1] 1.103912 # this is our estimate for "Implied Elasticities of Substitution, 1959" for Labor/Capital

There are slight deviations. They might come from using an updated dataset...?