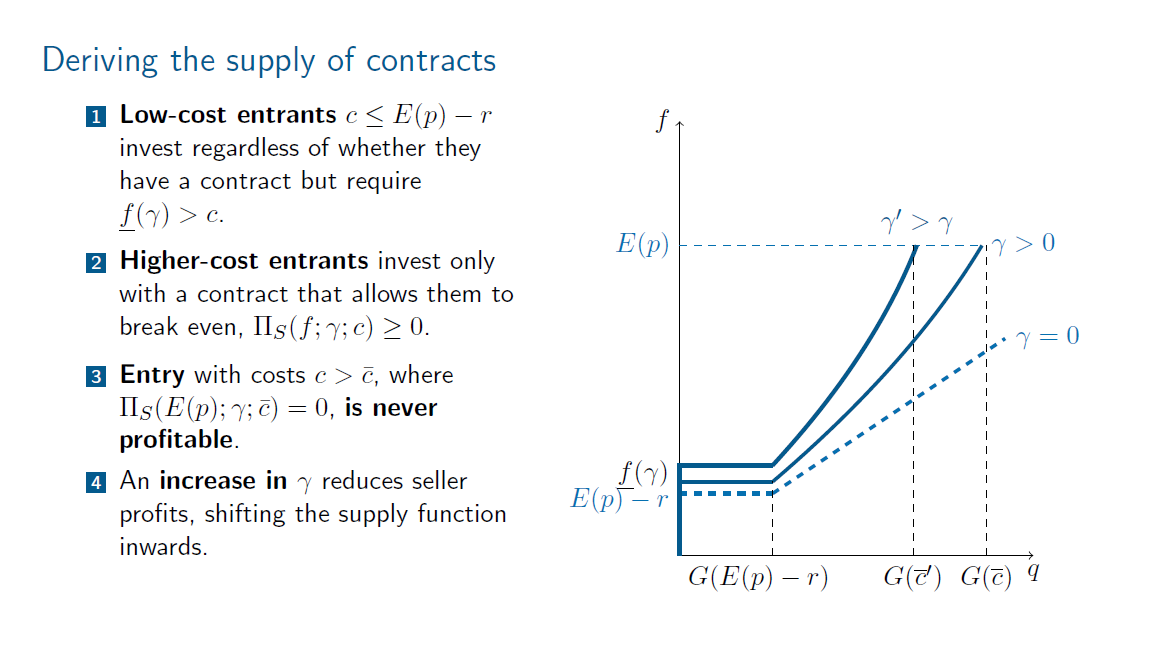

Hi Posit Community,

I am doing numerical methods and I am struggling to produce the PNG file that is enclosed:

Below is my code using reprex(), in which I try to replicate this, but obtained a completely different graph:

# Required libraries

if (!require("pacman")) install.packages("pacman")

pacman::p_load(ggplot2, tidyverse, hrbrthemes, gridExtra, cubature, formattable, rootSolve, readr, pracma, here, fs, truncdist, xtable, reshape2, writexl)

# Define the necessary functions

compute_R_gamma <- function(f, gamma, r, alpha, beta) {

# Handle boundary conditions

if (f == 0 || gamma == 0) {

return(0)

}

if (f == 1 && gamma == 1) {

return(r)

}

# Compute the variance of p

var_p <- (alpha * beta) / ((alpha + beta)^2 * (alpha + beta + 1))

# Function to calculate the variance of the minimum of p and f

var_tilde_p <- function(f, alpha, beta) {

# Define the PDF of the Beta distribution

beta_pdf <- function(p) dbeta(p, alpha, beta)

# Define the CDF of the Beta distribution

beta_cdf <- function(p) pbeta(p, alpha, beta)

# First moment of tilde_p (E[tilde_p])

first_moment <- integrate(function(p) {

p * beta_pdf(p)

}, lower = 0, upper = f)$value + f * (1 - beta_cdf(f))

# Second moment of tilde_p (E[tilde_p^2])

second_moment <- integrate(function(p) {

p^2 * beta_pdf(p)

}, lower = 0, upper = f)$value + f^2 * (1 - beta_cdf(f))

# Variance of tilde_p

second_moment - first_moment^2

}

# Compute the variance of tilde_p

var_tilde_p_value <- var_tilde_p(f, alpha, beta)

# Compute R_gamma(f, gamma)

R_gamma_value <- r * gamma^2 * (var_tilde_p_value / var_p)

return(R_gamma_value)

}

contract_market_profit <- function(f, gamma, c, r, alpha, beta) {

term1 <- f * (1 - gamma * pbeta(f, alpha, beta))

term2 <- gamma * integrate(function(p) p * dbeta(p, alpha, beta), lower = 0, upper = f)$value

term3 <- compute_R_gamma(f, gamma, r, alpha, beta)

return(term1 + term2 - term3 - c)

}

spot_market_profit <- function(c, mean_p, r) {

return(mean_p - r - c)

}

# Function to find f_underline by solving the equality of profits

find_f_underline <- function(c, gamma, r, alpha, beta, mean_p) {

# Define the function representing the difference in profits

profit_difference <- function(f) {

contract_market_profit(f, gamma, c, r, alpha, beta) - spot_market_profit(c, mean_p, r)

}

# Use uniroot to find the root of the profit difference function

result <- tryCatch(

uniroot(profit_difference, lower = mean_p - r, upper = mean_p)$root,

error = function(e) NA

)

# Ensure the found f_underline is greater than or equal to E(p) - r

if (!is.na(result) && result >= (mean_p - r)) {

return(result)

} else {

return(NA)

}

}

# Calculate the break-even investment cost c_break_even for a given gamma

find_c_break_even <- function(gamma, r, alpha, beta, mean_p) {

tryCatch(

uniroot(

function(c) contract_market_profit(mean_p, gamma, c, r, alpha, beta),

lower = 0, upper = 1 # Search interval for c, this could be adjusted depending on context

)$root,

error = function(e) NA

)

}

# Calculate the highest investment cost c_bar(gamma) for which entry might be profitable

find_c_bar <- function(gamma, r, alpha, beta, mean_p) {

# The highest investment cost such that the seller breaks even at f = E(p)

find_c_break_even(gamma, r, alpha, beta, mean_p)

}

# Categorize entrants based on their costs

categorize_entry <- function(c, gamma, r, alpha, beta, mean_p) {

# Calculate key thresholds

f_lower_bound <- mean_p - r # E(p) - r

c_bar <- find_c_bar(gamma, r, alpha, beta, mean_p)

# Check conditions for categorization

if (c > c_bar || is.na(c_bar)) {

return("No Entry (c > c_bar)")

} else if (c <= f_lower_bound) {

return("Low-Cost Entrant (c <= E(p) - r)")

} else {

return("Higher-Cost Entrant (c > E(p) - r)")

}

}

# Initialize parameters

c_values <- seq(0, 1, by = 0.05) # Example c values

gamma_values <- seq(0, 1, by = 0.1) # Example gamma values

alpha <- 4 # Alpha parameter of Beta distribution

beta <- 2 # Beta parameter of Beta distribution

r <- 0.4 # Risk premium

mean_p <- 0.6 # E(p)

# Generate results for all combinations of gamma and c

entry_results <- data.frame()

for (gamma in gamma_values) {

c_bar <- find_c_bar(gamma, r, alpha, beta, mean_p) # Compute c_bar

if (!is.na(c_bar)) {

for (c in c_values) {

# Compute specific f(gamma) using find_f_underline

f_specific <- find_f_underline(c, gamma, r, alpha, beta, mean_p)

# Compute E(p) - r (lower bound for low-cost entrants)

lower_f_gamma <- mean_p - r

# Compute profits in both markets

profit_spot <- spot_market_profit(c, mean_p, r)

profit_contract <- if (!is.na(f_specific)) {

contract_market_profit(f_specific, gamma, c, r, alpha, beta)

} else {

NA

}

# Entrant Type Logic (with explicit NA checks)

if (c > c_bar) {

entrant_type <- "No Entry (c > c_bar)"

} else if (c <= lower_f_gamma && !is.na(f_specific) && f_specific > c) {

entrant_type <- "Low-Cost Entrant (c <= E(p) - r)"

} else if (!is.na(profit_contract) && profit_contract >= c) {

entrant_type <- "Higher-Cost Entrant (c > E(p) - r)"

} else if (lower_f_gamma < c) {

entrant_type <- "f(gamma) < c"

} else {

entrant_type <- "Undefined"

}

# Store results in entry_results

entry_results <- rbind(

entry_results,

data.frame(

gamma = gamma,

c = c,

c_bar = c_bar,

f_specific = f_specific,

lower_f_gamma = lower_f_gamma,

profit_spot = profit_spot,

profit_contract = profit_contract,

profit_difference = profit_contract - profit_spot,

c_bar_normalized = pmin(c / c_bar, 1),

entrant_type = entrant_type

)

)

}

}

}

# Plot the results

ggplot(entry_results, aes(x = c_bar_normalized, y = f_specific, color = factor(gamma))) +

geom_line(linewidth = 1) +

geom_point(size = 2, alpha = 0.7) +

labs(

title = "Cumulative Supply G(c) vs Contract Prices f(gamma)",

x = "Cumulative Supply G(c)",

y = "Contract Price f(gamma)",

color = "Gamma (Proportion of Opportunistic Buyers)"

) +

theme_minimal() +

scale_color_brewer(palette = "Dark2")

# Print the results

print(entry_results)

and the graph obtained does not look at all at the one shown above.

Any ideas how I can obtain more or less the first figure shown above, please? Thank you so much.

Michael