Hi all,

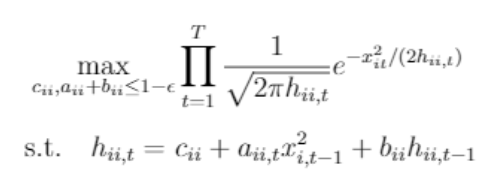

I am currently trying to implement a DVECH MGARCH model to a series of financial data. In order to do so, I have to maximize a quasi-likelihood function (see png). I have been looking for an adequate function for quite some time, unfortunately without any success. Does anybody know a package which contains such a function?

Thank you kindly for your suggestions.