I tried to write a real-time trading system, however do not know how to fit a Kelly model into the system. The system will automatically calculate everyday 12AM while I want to add another function which is auto placed order with certain stakes (by applied Kelly criterion model) once got the calculated forecast price.

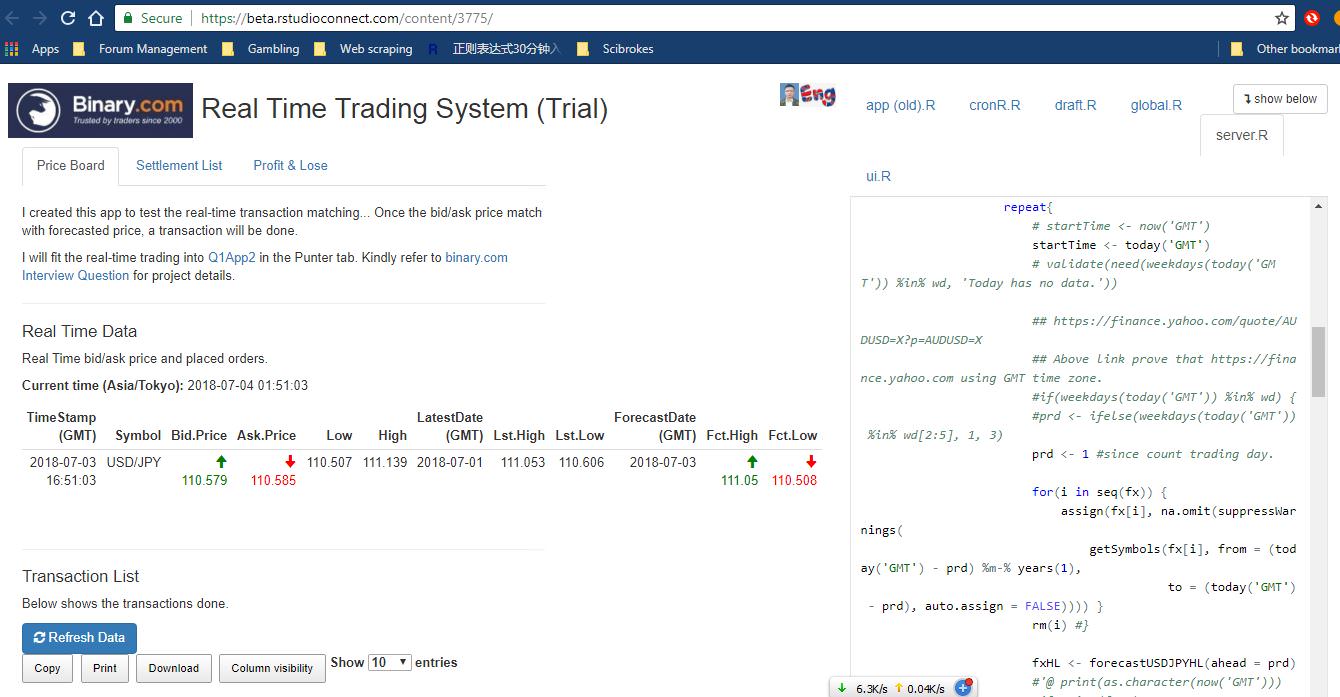

Source Code:Real Time Trading System (Trial)

Below coding is that I tried to use looping to calculate the data history, calculate the staking, profit & lose, and also bankroll.

...

...

...

## merge dataset

fitm <- cbind(fit1, forClose = fit2$Point.Forecast) %>% tbl_df

## convert to probability.

fitm %<>% mutate(ProbB = pnorm(Point.Forecast, mean = forClose, sd = sd(forClose)),

ProbS = 1 - ProbB) #ProbS = pnorm(Point.Forecast, mean = forClose, sd = sd(forClose), lower.tail = FALSE)

## The garch staking models (Kelly criterion) P&L column.

## staking model and bankroll management.

## need to refer to Niko Martinen's fund management formula to maximise the stakes and profit base on Kelly models.

## https://github.com/scibrokes/betting-strategy-and-model-validation/blob/master/references/Creating%20a%20Profitable%20Betting%20Strategy%20for%20Football%20by%20Using%20Statistical%20Modelling.pdf

#.... dynamic staking model need to adjusted based on updated bankroll but not portion of fixed USD100 per bet.

fitm %<>% mutate(BR = .initialFundSize) %>%

#'@ mutate(Return.Back = ifelse(Prob > 0.5, Diff * Back * stakes, 0),

#'@ Return.Lay = ifelse(Prob < 0.5, -Diff * Lay * stakes, 0))

mutate(fB = 2 * ProbB - 1, fS = 2 * ProbS - 1,

EUB = ProbB * log(BR * (1 + fB)) + (1 - ProbB) * log(BR * (1 - fB)),

EUS = ProbS * log(BR * (1 + fS)) + (1 - ProbS) * log(BR * (1 - fS)),

#'@ Edge = ifelse(f > 0, EUB, EUS), #For f > 0 need to buy and f <= 0 need to sell.

#need to study on the risk management on "predicted profit" and "real profit".

Edge = ifelse(fB > 0, EUB, ifelse(fS > 0, EUS, 0)),

PF = ifelse(Point.Forecast >= USDJPY.Low &

Point.Forecast <= USDJPY.High,

Point.Forecast, 0), #if forecasted place-bet price doesn't existing within Hi-Lo price, then the buying action is not stand. Assume there has no web bandwith delay.

FC = ifelse(forClose >= USDJPY.Low & forClose <= USDJPY.High,

forClose, USDJPY.Close), #if forecasted settle price doesn't existing within Hi-Lo price, then the closing action at closing price. Assume there has no web bandwith delay.

#'@ Diff = round(forClose - USDJPY.Close, 2),

##forecasted closed price minus real close price.

Buy = ifelse(PF > 0 & FC > PF, 1, 0), ##buy action

Sell = ifelse(PF > 0 & FC < PF, 1, 0), ##sell action

BuyS = Edge * Buy * (forClose - PF),

SellS = Edge * Sell * (PF - forClose),

Profit = BuyS + SellS, Bal = BR + Profit)

#'@ fitm %>% dplyr::select(Point.Forecast, forClose, Prob, BR, f, EU, Edge, PF, FC, Buy, Sell, SP, Bal)

#'@ fitm %>% dplyr::select(ProbB, ProbS, BR, fB, fS, EUB, EUS, Edge, PF, USDJPY.Open, FC, Buy, Sell, BuyS, SellS, Profit, Bal) %>% filter(PF > 0, FC > 0)

## The garch staking models (Kelly criterion) Adjusted Banl-roll and Balance column.

for(i in seq(2, nrow(fitm))) {

fitm$BR[i] = fitm$Bal[i - 1]

fitm$fB[i] = 2 * fitm$ProbB[i] - 1

fitm$fS[i] = 2 * fitm$ProbS[i] - 1

fitm$EUB[i] = fitm$ProbB[i] * log(fitm$BR[i] * (1 + fitm$fB[i])) +

(1 - fitm$ProbB[i]) * log(fitm$BR[i] * (1 - fitm$fB[i]))

fitm$EUS[i] = fitm$ProbS[i] * log(fitm$BR[i] * (1 + fitm$fS[i])) +

(1 - fitm$ProbS[i]) * log(fitm$BR[i] * (1 - fitm$fS[i]))

fitm$Edge[i] = ifelse(fitm$fB[i] > 0, fitm$EUB[i],

ifelse(fitm$fS[i] > 0, fitm$EUS[i], 0)) #For f > 0 need to buy and f <= 0 need to sell.

#need to study on the risk management on "predicted profit" and "real profit".

fitm$BuyS[i] = fitm$Edge[i] * fitm$Buy[i] * (fitm$forClose[i] - fitm$PF[i])

fitm$SellS[i] = fitm$Edge[i] * fitm$Sell[i] * (fitm$PF[i] - fitm$forClose[i])

fitm$Profit[i] = fitm$BuyS[i] + fitm$SellS[i]

fitm$Bal[i] = fitm$BR[i] + fitm$Profit[i]

#'@ if(fitm$Bal[i] <= 0) stop('All invested fund ruined!')

}; rm(i)

names(mbase) <- str_replace_all(names(mbase), '^(.*?)+\\.', nm)

if(.filterBets == TRUE) {

fitm %<>% filter(PF > 0, FC > 0)

}

fitm %<>% mutate(RR = Bal/BR)

## convert the log leverage value of fund size and profit into normal digital figure with exp().

if(.fundLeverageLog == TRUE) fitm %<>%

mutate(BR = exp(BR), BuyS = exp(BuyS), SellS = exp(SellS),

Profit = exp(Profit), Bal = exp(Profit))

return(fitm)

Source Code:simStakesGarch.R

Reference