Thanks for your answers,

So, i will try to explain with my weak english level ^^'

dCanada = diff(Canada,1)

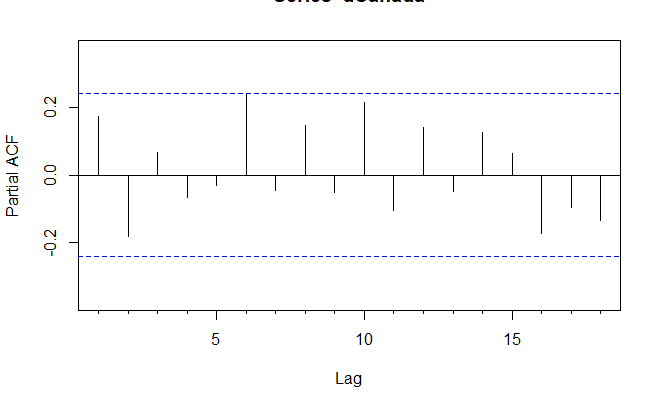

PACF(dCanada)

I diff my serie then i made PACF : i found a weak autocorrelation at order 6

EACF(dCanada)

Box.test(dCanada, lag=12 , type="Ljung-Box")

AR/MA

0 1 2 3 4 5 6 7 8 9 10 11 12 13

0 o o o o o o o o o o o o o o

1 x o o o o o o o o o o o o o

2 x x o o o o o o o o o o o o

3 x o o o o o o o o o o o o o

4 x o o x o o o o o o o o o o

5 o o o x o x o o o o o o o o

6 o x o o o o o o o o o o o o

7 x x o o o o o o o o o o o o

Box-Ljung test

data: dCanada

X-squared = 10.216, df = 12, p-value = 0.597

**So , i made EACF and found a ARMA(0,0) .... really weird... **

Moreover, LB test at lag 12 have p-value > 0.05 ......

auto.arima(dCanada, trace=TRUE, ic=c("aic"))

ARIMA(2,0,2) with non-zero mean : Inf

ARIMA(0,0,0) with non-zero mean : 175.2989

ARIMA(1,0,0) with non-zero mean : 175.3013

ARIMA(0,0,1) with non-zero mean : 174.2514

ARIMA(0,0,0) with zero mean : 173.3635

ARIMA(1,0,1) with non-zero mean : 175.4723

Best model: ARIMA(0,0,0) with zero mean

Series: dCanada

ARIMA(0,0,0) with zero mean

sigma^2 estimated as 0.7855: log likelihood=-85.68

AIC=173.36 AICc=173.43 BIC=175.55

So, i decide to make an auto.arima et found ARIMA(0,0,0) with non mean as best model....

But i wasn't convinced by this model because i founded autocorrelation with PACF...

So i test a lot of model and found ARMA(2,2) with a better AIC than the ARMA(0,0) ...

ARMA0_0 = Arima(dCanada, order = c(0,0,0), include.mean=FALSE)

ARMA2_2 = Arima(dCanada, order = c(2,0,2), include.mean=FALSE)

coeftest(ARMA2_2)

AIC(ARMA2_2)

AIC(ARMA0_0)

z test of coefficients:

Estimate Std. Error z value Pr(>|z|)

ar1 -1.460105 0.114566 -12.7447 < 2.2e-16 ***

ar2 -0.493069 0.113722 -4.3357 1.453e-05 ***

ma1 1.944239 0.068811 28.2549 < 2.2e-16 ***

ma2 0.999974 0.069793 14.3278 < 2.2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

[1] 166.2296

[1] 173.3635

My forecast seems to be very good with the ARMA(2,2) and all white noise hypothesis IS OK with it.

How can i be sure ARMA(2,2) is the best model ? Why auto.arima don't give me the ARIMA(2,0,2) model directly ?

Can i found better with an AR(6) ? Or MA(6) ?

Thanks,

Paul