My study is about the influence of board diversity (gender and age) and fund size on the voting behavior of pension funds. I have also included control variables that concern the board type, board size, fund type, and also control for time.

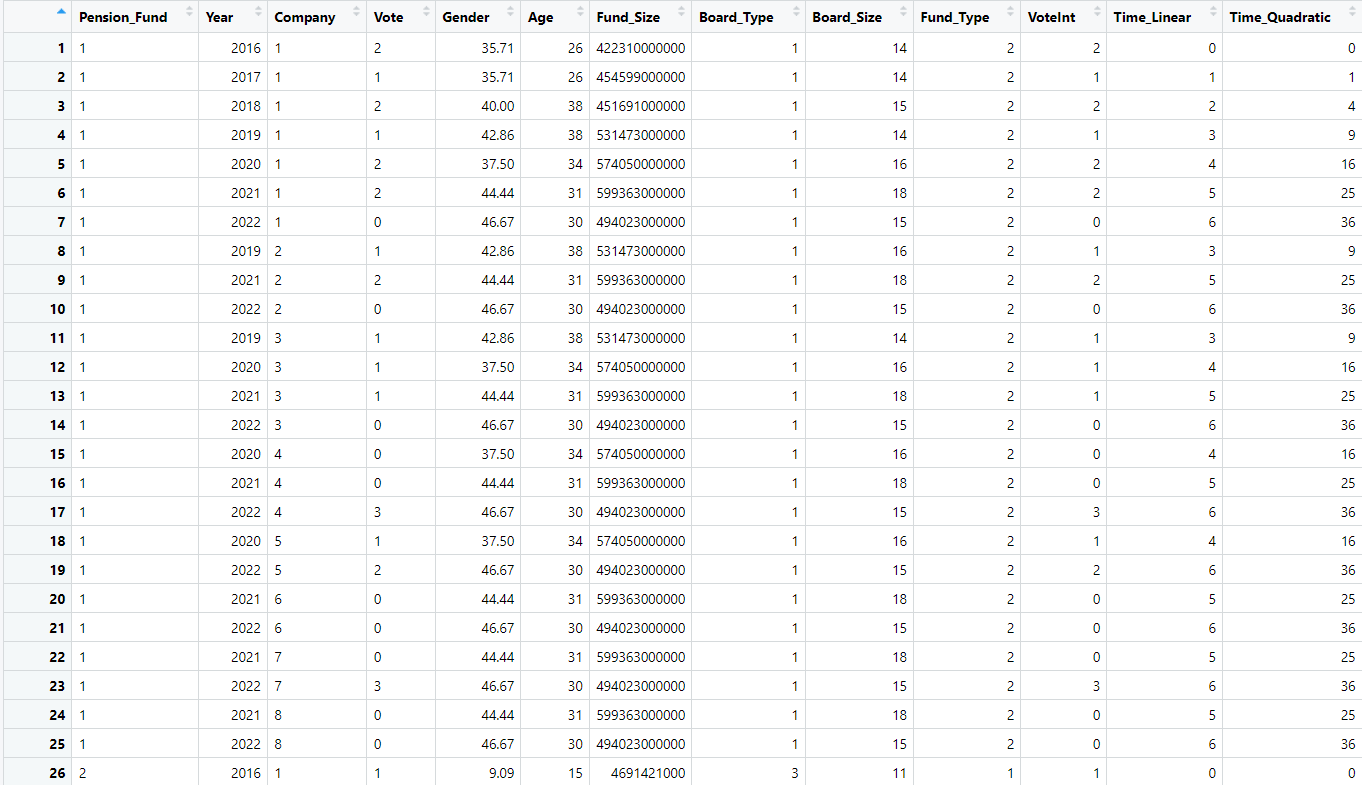

This is only a snippet, but I have data on 38 pension funds who have voted on 8 different companies across multiple years. This is why I included random effects (my observations are not independent from each other). Furthermore, Vote is the dependent variable and Gender, Age, Fund_Size are my independent variables. My code looks like this:

gam(list(VoteInt ~ Gender + Age + Board_Size + Board_Type + Fund_Type + Time_Linear + s(Pension_Fund, bs = "re") + s(Company, bs = "re"),

~ Gender + Age + Board_Size + Board_Type + Fund_Type + Time_Linear + s(Pension_Fund, bs = "re") + s(Company, bs = "re"),

~ Gender + Age + Board_Size+ Board_Type+ Fund_Type+ Time_Linear+ s(Pension_Fund, bs = "re")+ s(Company, bs = "re"),

~ Gender + Age + Board_Size+ Board_Type+ Fund_Type+ Time_Linear+ s(Pension_Fund, bs = "re")+ s(Company, bs = "re")),

family = multinom(K = 4), data = Data_FINAL)

And the summary of my model looks like this:

Family: multinom

Link function:

Formula:

`VoteInt ~ Gender + Age + Board_Size + Board_Type + Fund_Type + Time_Linear + Time_Quadratic + s(Pension_Fund, bs = "re") + s(Company, bs = "re") ~ Gender + Age + Board_Size + Board_Type + Fund_Type + Time_Linear + Time_Quadratic + s(Pension_Fund, bs = "re") + s(Company, bs = "re")

~Gender + Age + Board_Size + Board_Type + Fund_Type + Time_Linear + Time_Quadratic + s(Pension_Fund, bs = "re") + s(Company, bs = "re") ~ Gender + Age + Board_Size + Board_Type + Fund_Type + Time_Linear + Time_Quadratic + s(Pension_Fund, bs = "re") + s(Company, bs = "re")`

Parametric coefficients:

Estimate Std. Error z value Pr(>|z|)

(Intercept) 4.466425 1.660200 2.690 0.00714 **

Gender -0.004713 0.017598 -0.268 0.78886

Age -0.072018 0.028087 -2.564 0.01034 *

Board_Size 0.059774 0.097628 0.612 0.54036

Board_Type 0.371302 0.207263 1.791 0.07322 .

Fund_Type -0.690773 0.593078 -1.165 0.24413

Time_Linear -0.870433 0.331964 -2.622 0.00874 **

Time_Quadratic -0.012734 0.044390 -0.287 0.77421

(Intercept).1 1.608973 1.179053 1.365 0.17237

Gender.1 -0.002788 0.013254 -0.210 0.83340

Age.1 -0.058961 0.022502 -2.620 0.00879 **

Board_Size.1 0.081464 0.069461 1.173 0.24088

Board_Type.1 0.317223 0.121651 2.608 0.00912 **

Fund_Type.1 -0.190059 0.350472 -0.542 0.58762

Time_Linear.1 -0.089743 0.315876 -0.284 0.77633

Time_Quadratic.1 -0.067089 0.040601 -1.652 0.09846 .

(Intercept).2 -4.069578 2.807917 -1.449 0.14725

Gender.2 0.013059 0.025064 0.521 0.60234

Age.2 0.003533 0.039827 0.089 0.92930

Board_Size.2 -0.298899 0.145000 -2.061 0.03927 *

Board_Type.2 -0.025187 0.281487 -0.089 0.92870

Fund_Type.2 1.290481 0.802374 1.608 0.10776

Time_Linear.2 0.010836 0.830649 0.013 0.98959

Time_Quadratic.2 0.083271 0.090332 0.922 0.35661

(Intercept).3 -0.994601 2.515822 -0.395 0.69259

Gender.3 -0.018943 0.019669 -0.963 0.33548

Age.3 -0.035921 0.044371 -0.810 0.41819

Board_Size.3 0.113424 0.120216 0.943 0.34543

Board_Type.3 -0.109712 0.289897 -0.378 0.70510

Fund_Type.3 0.247172 0.970303 0.255 0.79893

Time_Linear.3 -0.675938 0.462838 -1.460 0.14417

Time_Quadratic.3 0.106795 0.055379 1.928 0.05380 .

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Approximate significance of smooth terms:

edf Ref.df Chi.sq p-value

s(Pension_Fund) 27.916 36 243.74 < 2e-16 ***

s(Company) 4.190 7 11.61 0.0447 *

s.1(Pension_Fund) 21.872 36 148.00 9.49e-06 ***

s.1(Company) 4.233 7 14.48 0.0189 *

s.2(Pension_Fund) 24.770 36 206.25 7.76e-06 ***

s.2(Company) 5.970 7 47.77 6.43e-06 ***

s.3(Pension_Fund) 29.069 36 499.22 < 2e-16 ***

s.3(Company) 6.320 7 147.71 < 2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Deviance explained = 44.6%

-REML = 708.93 Scale est. = 1 n = 950

I checked the validity of my model by performing test for multicollinearity, heteroscedasticity, and the distribution of my residuals (by using VIF, the White test, and the Shapiro-Wilk test). I get the following results:

VIF(model):

Gender Age Board_Size Board_Type

1.276704 1.066428 1.225880 1.056866

Fund_Type Time_Linear Time_Quadratic

1.058455 15.856650 15.553722

the White test:

studentized Breusch-Pagan test

data: model

BP = 142.44, df = 7, p-value < 2.2e-16

Shapiro-Wilk test:

Shapiro-Wilk normality test

data: model$residuals

W = 0.91792, p-value < 2.2e-16

I tried to resolve the heteroscedasticity and the non-normality distribution of the residuals by robust regression but it did not work. Does anyone know how I can solve this?