I am writing a seminar paper on portfolio insurance strategies and how each of them performs in a Monte Carlo Simulation under the assumption of Cumulative Prospect Theory (CPT) investors.

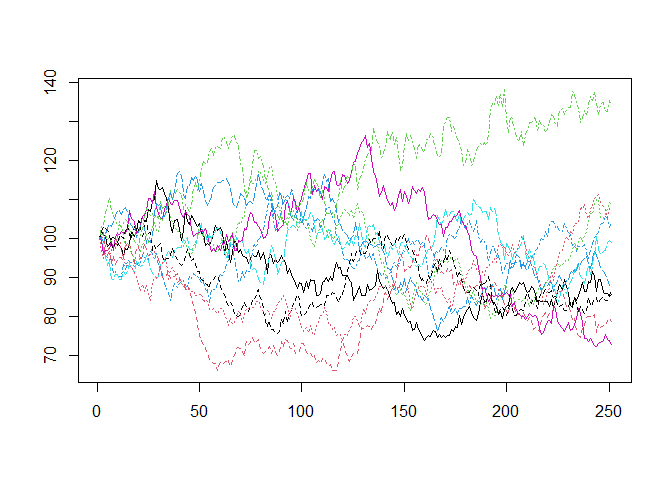

For that, I am currently trying to program the simulation in R. The simulation is supposed to simulate 250 daily stock market returns and the continuously compounded stock market returns should be generated using the Geometric Brownian motion. There is also four different stock market scenarios that need to be considered. In the first, the risk premium is 4.5% and the volatility is 20%. In the second, the risk premium is 7% and the volatility is 20%. In the third, the risk premium is 4.5% and the volatility is 30%. In the fourth scenario, the risk premium is 7% and the volatility is 30%. I do not know how to incorporate all of that in the simulation. So my question is, how do I program the Monte Carlo Simulation so that it uses the Geometric Brownian motion to generate continuously compounded stock market returns and takes the different stock market returns into account. The simulation should be run for each stock market scenario, so a comparison of the performance of the portfolio insurance strategies in the different market scenarios is possible. The portfolio insurance strategies are Buy-and-Hold, Constant-Proportion-Portfolio-Insurance, Stop-Loss and Synthetic-Put.