Hello

Why do we get NAs in residual and fitted values of forecast() function. Below is an example

fancy <- scan("http://robjhyndman.com/tsdldata/data/fancy.dat")

souvenir_series = ts(data =log(fancy),start = 1987, frequency = 12)

souvenir_series_forecasts = HoltWinters(souvenir_series)

souvenir_series_forecasts2 = forecast(souvenir_series_forecasts,h = 48)

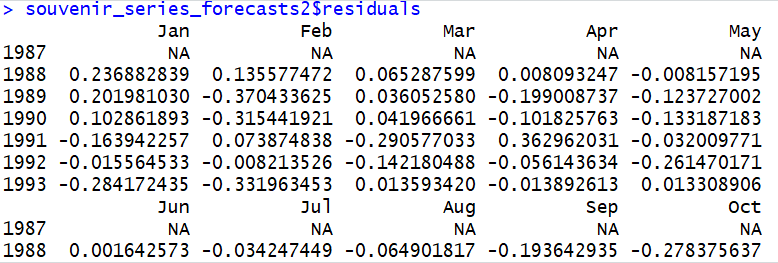

souvenir_series_forecasts2$residuals

Andrea

April 16, 2019, 11:06am

3

Hi!

To help us help you, could you please prepare a repr oducible ex ample (reprex) illustrating your issue? Please have a look at this guide, to see how to create one:

A minimal reproducible example consists of the following items:

A minimal dataset, necessary to reproduce the issue

The minimal runnable code necessary to reproduce the issue, which can be run

on the given dataset, and including the necessary information on the used packages.

Let's quickly go over each one of these with examples:

By executing the codes which I have given, you will be able to generate the output shown.

Let me know if I am missing something.

Andrea

April 16, 2019, 12:27pm

5

I won't, because your code doesn't load any package. Please have a look at the link I provided to see how to make a reproducible example.

system

May 7, 2019, 12:27pm

6

This topic was automatically closed 21 days after the last reply. New replies are no longer allowed.