Hello all,

I tried to initate a forecast in working with tsibbles and the fable package. My forecast result is sadly not very good, and I wanted to make sure that the reason for that is the problem with my stats and the data and not my R code. In hilo i see that the outpur is the same for every row of the value which makes me think that the model might be not working.

Data source: Ethereum Price | ETH Price Index and Live Chart — CoinDesk 20

library(feasts) # working with tsibbles

library(tsibble)

library(fable) #for tsibble flow eps and so on

library(tidyverse)

#library(dplyr) included tidyverse

#library(ggplot2) included tidyverse

library(lubridate) #date transformation package

library(magrittr) # advanced pipeing

library(sweep) #helps in working with ets objects for vizulasiation and transformation brings ts in tidyworkflow

csv_data_1 <- read.csv("ETH_USD_CoinDesk.csv")

z_eth <- mutate(csv_data_1, Currency = NULL, X24h.High..USD. = NULL, X24h.Low..USD.=NULL, X24h.Open..USD.=NULL) %>%

mutate(Date = yearmonth(Date)) %>% group_by(Date) %>% summarise(avgPM = mean(Closing.Price..USD.)) %>% as_tsibble(index = Date)

z_eth %>% #TSIBBLE

autoplot() +

labs(y = "Closing price", x="Date")

z_eth %>% gg_season(avgPM)

z_eth_deco <- z_eth %>% model(STL(avgPM)) #MABLE

z_eth_test <- z_eth %>% slice(1:floor(.75nrow(z_eth)))

z_eth_out <- z_eth %>% slice((floor(.75nrow(z_eth)):n()))

z_eth_deco %>%

gg_tsresiduals()

moreDat <- z_eth_deco %>% augment

moreDat %>% features(.innov, box_pierce, lag = 10, dof = 0)

moreDat %>% autoplot(.innov) + ylab("Residuals")

xDec <- z_eth %>% features(avgPM, feat_stl)

components(z_eth_deco) %>% as_tsibble() %>% autoplot(avgPM) +

geom_line(aes(y=trend), colour = "#D55E00") + #Why it shows seasonality if there is none.

geom_line(aes(y=remainder), colour = "blue") +

geom_line(aes(y=season_year), colour = "red")

ets_mod <- z_eth_test %>%

model(ets = ETS(avgPM ~ error("N") + trend("M") + season("N")))

ets_mod_auto <- z_eth_test %>%

model(ets = ETS(avgPM))

ets_mod_auto %>% report()

forecastLen <- length(z_eth_out$avgPM)

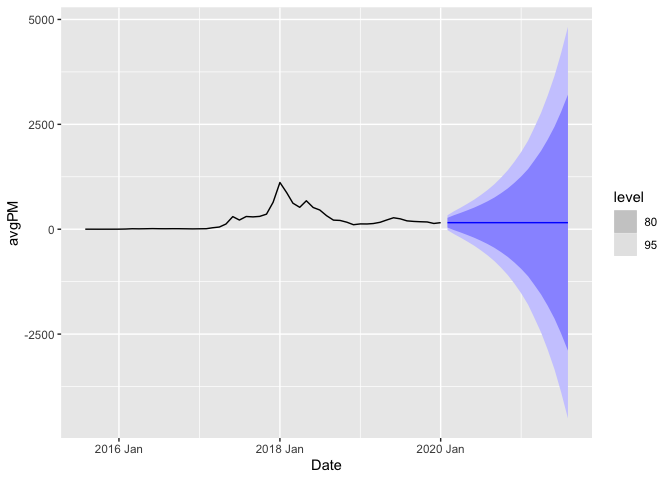

fc <- ets_mod_auto %>% forecast(h = forecastLen) #use namespace to not confuse with other packages ::

fc %>% autoplot()

fc %>%

hilo(level = c(80, 95))

fc %>% autoplot(z_eth_test)