Hi,

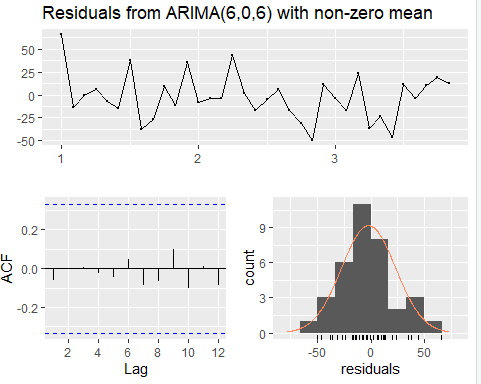

I'm working with ARIMA model and I checked the residuals and threw this.

What does non-zero mean? Is the model not valid for forecasting?

Hi,

I'm working with ARIMA model and I checked the residuals and threw this.

What does non-zero mean? Is the model not valid for forecasting?

See Section 3.3 in Forecasting Principles and Practices, 2nd ed.. Generally, residual diagnostics give insight into the possible opportunity to improve the model. It's desirable to have the residuals normally distributed with a mean of zero, but failure isn't necessarily fatal. The histogram shows the data to be 1) left skewed, but 2) having a small n. The short bar on the right "should" be taller. Because the ACF plot is good, I would compare this model against the naive, mean, random walk with drift and seasonal naive baseline models to see if it beats the RMSE or other statistic, then decide if the accuracy is satisfactory.

Your data (not the residuals) has a mean that is not zero, that is all. If you are using the auto.arima() function in the {forecast} package, which is what the online book referenced by technocrat uses, it will report this and show the estimated mean in the results. Look at the US consumption expenditure example in Section 8.5. You will notice that the forecast in the chart is about 0.75, which is close to the 0.745 estimated mean.

The third edition of the book uses the tidyverts set of packages instead. It reports the constant in the ARMA equation (after differencing), which is related to the mean. A non-zero constant (c) implies a non-zero mean (m). For AR(1), c = m x (1 - alpha).

This topic was automatically closed 21 days after the last reply. New replies are no longer allowed.

If you have a query related to it or one of the replies, start a new topic and refer back with a link.