Hello, everyone,

I have a question regarding the DIfferencing for an ARIMA model. In the first step I transform the data with:

Box.test(bc_ts, type="Ljung")

The next step is to give me

ndiffs(bc_ts)

that I need to differentiate the time series, which I will do in the next step:

diff_ts <- diff(bc_ts, differences = ndiffs(bc_ts))

After this, I will run auto.arima() as normal. Afterward I would like to test the accuracy and superimpose the graphs. First I transform the data back with BoxCox:

InvBoxCox(finalarima$x, lambda = lambda)

However, I don't know how to differentiate the data back to make the models comparable and plot them on top of each other. Unfortunately, I can't find a function to calculate back the forecasting series to get the total values. Enclosed once again my model.

I highly appreciate your help and best regards

Luke

# STEP 1: Check Volitality

# Box-Cox Transformation

lambda <- BoxCox.lambda(ts)

bc_ts <- BoxCox(ts,lambda=lambda)

tsdisplay(BoxCox(ts,lambda), ylab="Box Cox Transformed Demand")

# STEP 2: Detect Non-Stationary Data

# Box-Ljung test (tests the null hypothesis of absence of serial correlation)

Box.test(bc_ts, type="Ljung")

# ADF Test (non-stationary)

adf.test(bc_ts)

#KPSS Test (stationarity)

kpss.test(bc_ts)

kpss.test(diff(bc_ts))

# STEP 3: Differencing Non-Stationary Data

ndiffs(bc_ts)

diff_ts <- diff(bc_ts, differences = ndiffs(bc_ts))

plot.ts (diff_ts, ylab="Differenced & Box Cox Transformed Demand")

# STEP 4: Model Identification and Estimation

# METHOD: Minimum AIC/BIC Criteria

new_train <- window(diff_ts,

start = c(2016, 2),

end = c(2018, 52))

new_test <- window(diff_ts,

start = c(2019, 1),

end = c(2019, 52))

ARIMA <- auto.arima(new_train, trace=TRUE, ic="aicc", approximation = FALSE)

summary (ARIMA)

# Multi-step forecasts, re-estimation, 1-steps ahead

ARIMA_order <- arimaorder(ARIMA)

ARIMA_mat <- matrix(0, nrow=n, ncol=h)

for(i in 1:n)

{

x <- window(diff_ts, end=c(2018, 52) + (i-1)/52)

refit <- Arima(x, model=ARIMA)

ARIMA_mat[i,] <- forecast(refit, h=h)$mean

}

ARIMA_mat2 <- ts(ARIMA_mat, start=c(2019,1), end=c(2019,52), frequency=52)

IBC_ARIMA <- InvBoxCox(ARIMA_mat2, lambda=lambda)

#HOW TO BACKDIFFERENTIATE?

accuracy(IBC_ARIMA, test)

IBC_ARIMA %>% autoplot()

bind_ARIMA <- bind_cols(IBC_ARIMA, test)

colnames(bind_ARIMA) <- c("ARIMA_mat2","test")

bind_ARIMA2 <- bind_ARIMA %>%

mutate(week = 1:nrow(ARIMA_mat2)) %>%

gather(type, value, 1:2)

bind_ARIMA2

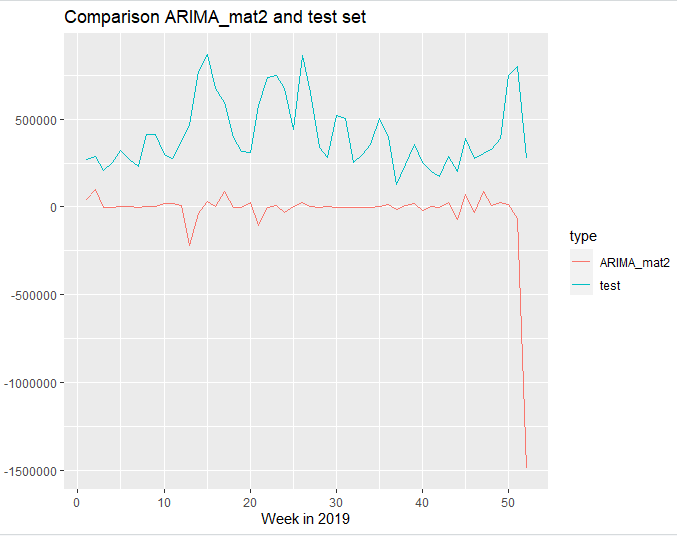

ggplot(data=bind_ARIMA2, mapping=aes(x=week, y=value, colour=type)) +

geom_line() + ggtitle("Comparison ARIMA_mat2 and test set") +

ylab ("Value") + xlab("Week in 2019")

In the end, the Plot looks like this: