Fitch92

1

Hello,

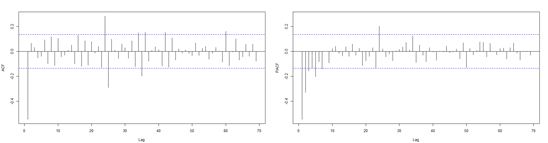

I just plotted my ACF and PACF Plot after differentiating the time series.

I as well used the auto.arima() function to get the final model. I therefore received:

for AIC:

ARIMA(0,1,2)(1,0,0)[52]

for BIC:

ARIMA(1,1,1)

I actually have no idea how one should read the plots to get these results. For me its a little contrary.

Can you help me?

Thank you in advance.

??forecast::auto.arimawill auto use the best c(p, d, q)

Here is example binary.com 面试试题 I - GARCH 模型中的 ARIMA(p,d,q) 参数最优化

I know, but I actually don`t get how forecast::auto.arima gets these values just from looking at the ACF and PACF plots

system

Closed

4

This topic was automatically closed 21 days after the last reply. New replies are no longer allowed.

If you have a query related to it or one of the replies, start a new topic and refer back with a link.