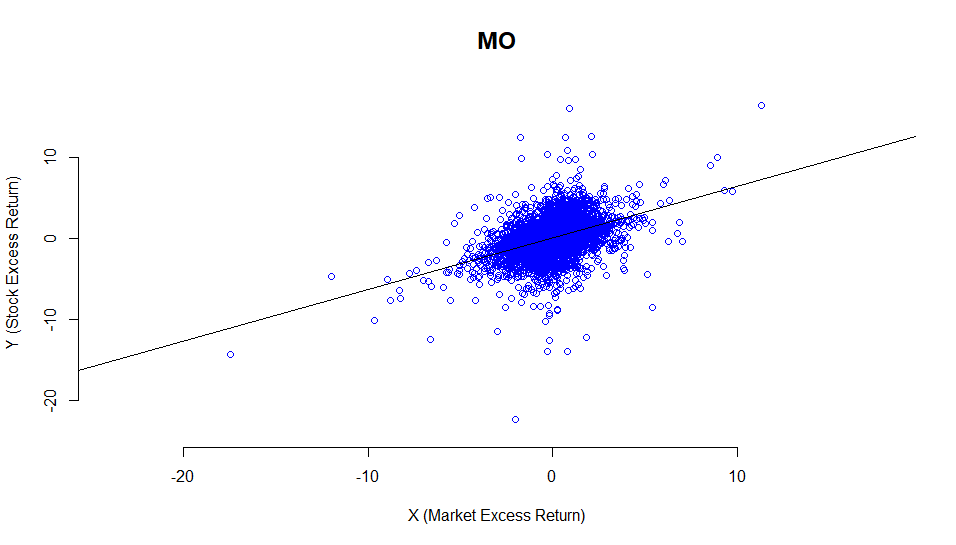

If stock holds and xts of my stock return data, and Market holds an xts of market return data, For the CAPM regression, I simply use:

CAPMreg <- lm(Stock ~ Market)

plot(

as.zoo(Market),

as.zoo(Stock),

xlab = "X (Market Excess Return)",

ylab = "Y (Stock Excess Return)",

cex.main = 1.5,

frame.plot = FALSE,

col = "blue"

) ## col=ifelse((x*y<0), "red", "blue")

abline(CAPMreg)

done - I get a beautiful plot: